คลิกเพื่ออ่านบทความฉบับภาษาไทย

Not the operators — the enablers

The demand case for Thailand’s data center buildout is clear. Less obvious is where the opportunity lies. Most investors are watching the hyperscalers. The more interesting question is who builds, connects, and commissions the facilities they need, and for Uncovered Thai Stocks, that is an interesting place to dig further.

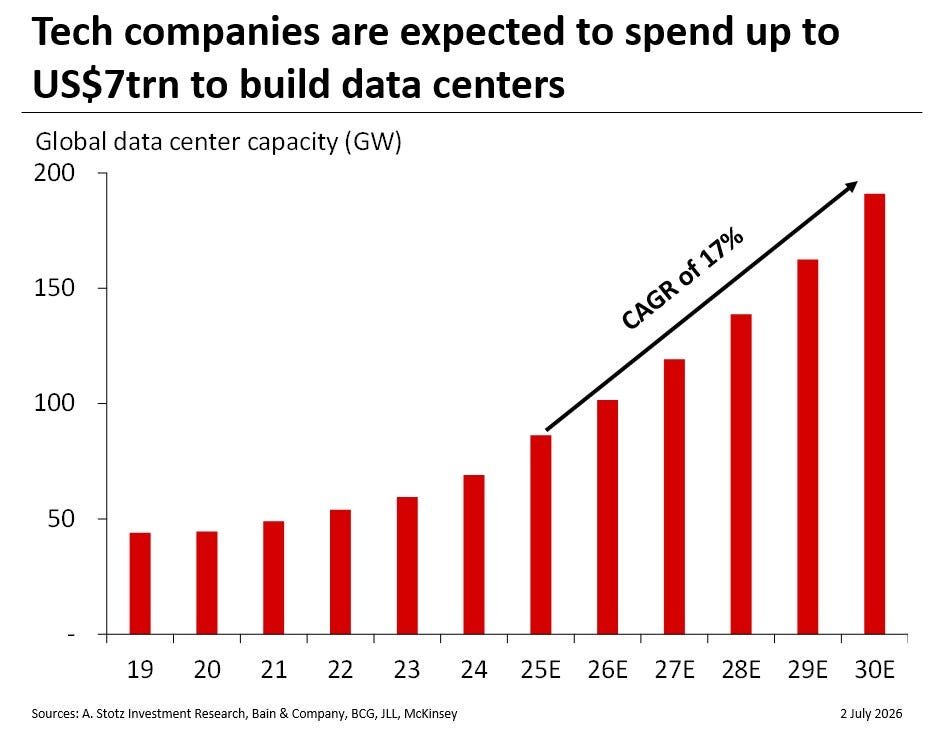

A boom measured in watts

Tech companies are expected to spend up to US$7 trillion building data centers over the coming years, with global capacity forecast to grow at a 17% CAGR, from around 80 gigawatts (GW) in 2025 to roughly 190 GW by 2030. AI is the primary driver, pushing demand for compute power well beyond existing infrastructure.

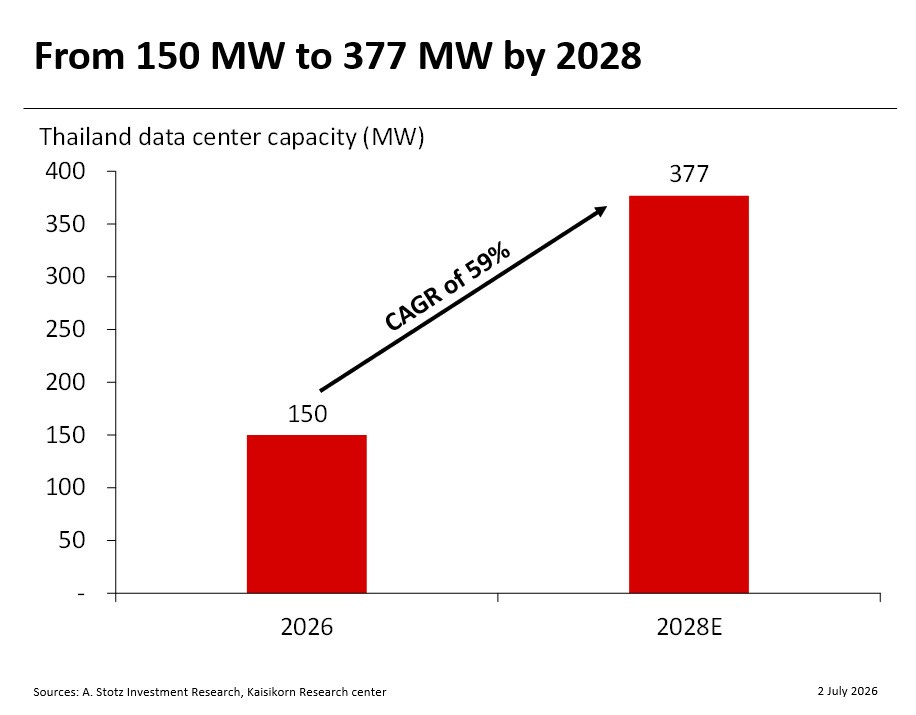

Thailand steps up

Thailand is emerging as one of Southeast Asia’s key destinations for that capital. According to KResearch, current live data center capacity in Thailand stands at 150 megawatts (MW), with a further 227 MW under construction and due online by 2028, representing a 59% compound annual growth rate (CAGR). The Eastern Economic Corridor (EEC) is rapidly emerging as the primary construction hub.

Big tech drives the buildout

The demand is coming from the world’s largest technology companies. AWS has pledged US$5bn, Google US$1bn, and ByteDance has committed US$8.8bn in data center investment, with a further US$25bn BOI-approved expansion announced in May 2026.

BMI’s June 2026 report describes Thailand as “Southeast Asia’s most improved data center market,” transitioning rapidly from early-stage interest to large-scale hyperscaler commitments.

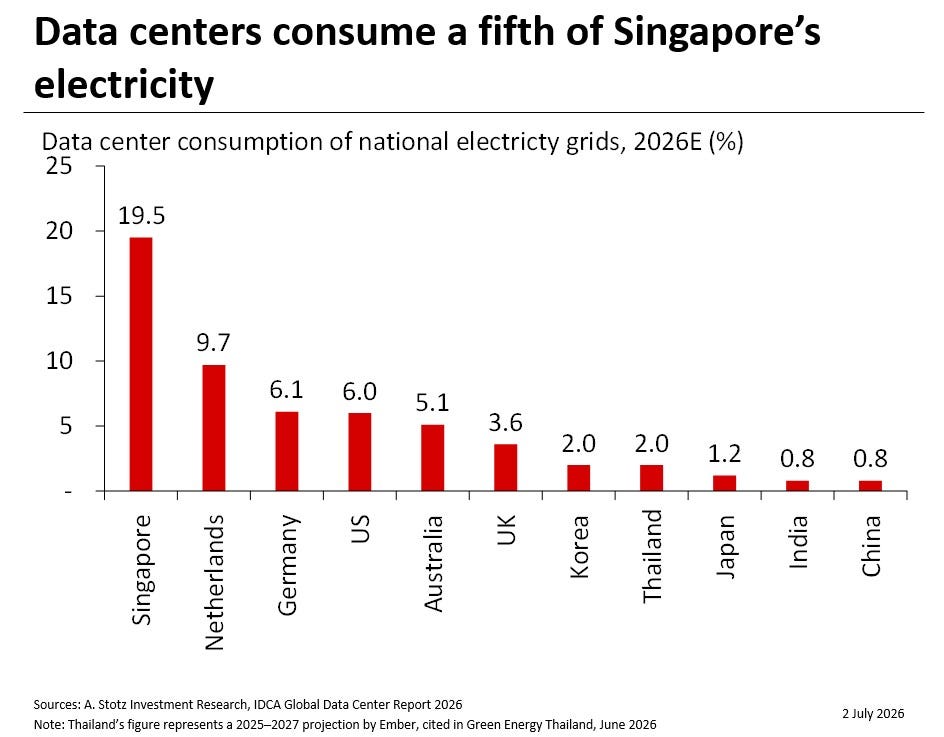

Singapore’s loss, Thailand’s gain

Data centers already consume an estimated 19.5% of Singapore’s national electricity grid, by far the highest share of any country in the world. The restrictions on new construction were not surprising.

Those restrictions have redirected billions of dollars of investment into neighboring markets. Thailand has been a primary beneficiary, helped by targeted BOI incentives.

The grid is the bottleneck

Grid readiness is the central execution risk. EEC substations are already running at or near capacity, causing delays. The gap between announced and operational capacity could widen if constraints are not resolved. Thailand has plenty of demand. What the country needs now is the grid to match it.

Looking past the large caps

Most investor attention on this theme focuses on the large-cap operators: GULF, TRUE, ADVANC, BGRIM, WHA, AMATA, and DELTA. But among our Top 50 Uncovered Thai Stocks, we have identified five companies with exposure to the buildout that have largely gone unnoticed.

Floyd PCL (FLOYD): Mechanical, electrical, and plumbing (MEP) systems

Every data center needs precision cooling, backup power, fire suppression, and building management systems. This is exactly what FLOYD does. Data center MEP installation is a revenue category in its financial reporting.

Read our 1Q26 report | Read between the lines

Syntec Construction (SYNTEC): Civil construction

SYNTEC has a dedicated data center construction team and a completed Tier 3 facility on record: the Osprey Data Center for OneAsia in Navanakorn Industrial Estate, 20,000 sq m at Bt455m. Mordor Intelligence names SYNTEC specifically in its Thailand data center construction market report.

Read our 1Q26 report | Read between the lines

Symphony Communication (SYMC): Fiber, submarine cable, colocation

SYMC operates a nationwide fiber backbone, its own submarine cable network, and data center colocation at AIMS@Bangkok, and, in November 2025, partnered with Telehouse Thailand to extend customer reach to Japan, Singapore, Hong Kong, and Europe.

Read our 1Q26 report | Read between the lines

ALT Telecom (ALT): Fiber and subsea infrastructure

ALT builds and leases fiber-optic networks and submarine cable infrastructure through its subsidiary, International Gateway Company (IGC), which operates 12,000 km of nationwide optical fiber and has access to five cable landing stations. In November 2025, Google selected IGC as its landing partner for the TalayLink submarine cable, connecting Thailand to Australia.

Read our 1Q26 report | Read between the lines

Advanced Information Technology (AIT): IT systems integration

Once a data center is built and the MEP systems are in place, the IT infrastructure must be commissioned. AIT is an established ICT system integrator with 30 years of experience, seven nationwide service centers, and Data Center and Cloud Solutions as a standalone named product line.

Read our 1Q26 report | Read between the lines

Five companies, one supply chain

These five companies sit at different points in the data center supply chain: civil construction, MEP installation, IT systems integration, fiber connectivity, and subsea cable. None of them owns or operates data centers. But every data center being built in Thailand needs all five of these capabilities. The exposure is real, verifiable, and in several cases already tied to active contracts, without the market attention that the headline names attract.

This is not a recommendation or investment advice. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied, is made regarding future performance.