คลิกเพื่ออ่านบทความฉบับภาษาไทย

Thailand’s economy shifted in important ways between April 2026 and early May 2026: an upgrade in credit outlook, lower growth forecasts, a dovish central bank, strong fuel price action, and the end of a year-long deflation streak. Each potentially shapes how Thai equities are being priced today.

1. Moody’s upgrades Thailand’s outlook to stable

On April 21, Moody’s raised Thailand’s sovereign outlook from negative to stable while keeping the Baa1 rating. This reversed last year’s downgrade. The agency pointed to lower tariff risk, as US duties on Thai exports now align with those of regional peers, and recovering investment. PM Anutin Charnvirakul’s February 2026 election win also eased political concerns.

A stable outlook lowers sovereign risk and is generally supportive of valuations, especially for banks and large caps. Whether it is enough to bring foreign flows back is the real test.

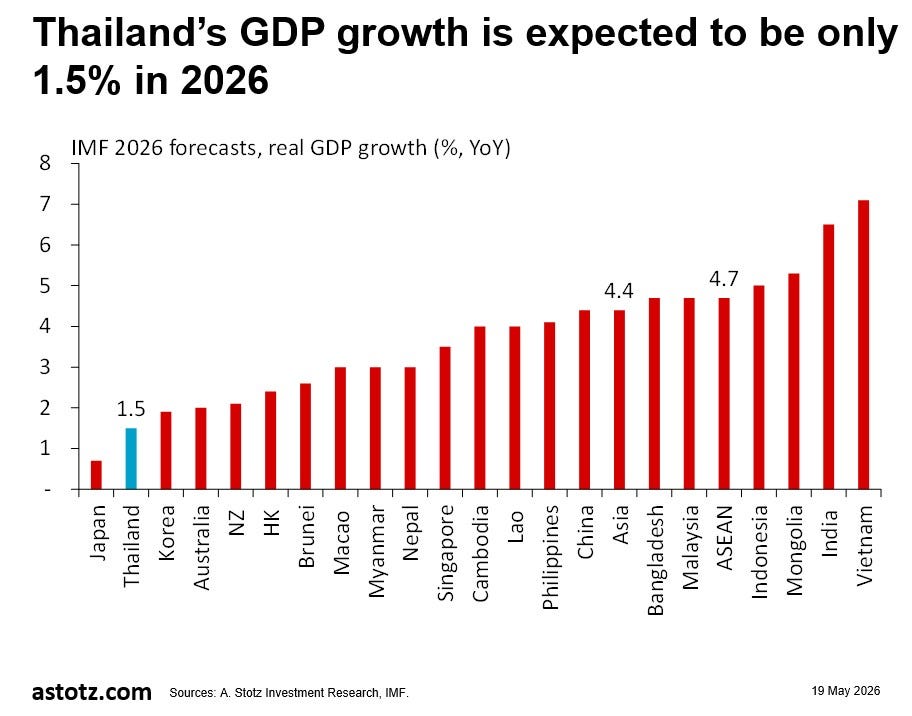

2. Growth forecasts cut across the board

Every major institution lowered its 2026 outlook for Thailand in April. The IMF cut its forecast to 1.5%, the World Bank to 1.3%, and the ADB to 1.8%. Both the Bank of Thailand (BOT) and Moody’s project 1.5%. The World Bank flagged Thailand as one of Southeast Asia’s most exposed economies to the energy shock.

On May 5, the Cabinet approved an emergency Bt400bn borrowing decree, split into Bt200bn for grassroots support, SMEs, and vulnerable groups, and Bt200bn for energy transition projects. BOT Governor Vitai Ratanakorn has warned that spending must be tightly targeted because broad relief simply raises the base and lowers measured growth the following year.

Where the Bt400bn actually lands will determine who benefits. Domestic consumer and SME-linked names are best placed if it’s well-targeted.

3. BOT holds at 1%, choosing growth over inflation

On April 29, the Monetary Policy Committee (MPC) voted unanimously to hold the policy rate at 1%, the lowest since September 2022. The MPC described the rise in inflation as supply-driven, and therefore not a problem that tighter policy can solve.

Updated forecasts project GDP growth of 1.5% in 2026 and 2% in 2027, with headline inflation averaging 2.9% this year before easing to 1.5%. Inflation is expected to remain above the 1–3% target range “for some time,” but the BOT does not view the move as broad enough to warrant action. With six cuts totaling 1.5% since October 2024, there is limited room to ease further.

Keeping rates low for longer can squeeze banks’ net interest margins, while rate-sensitive sectors such as property keep a modest lift.

4. Strong fuel price intervention

On April 23, EPPO approved a 5 baht per liter cut at the refinery gate, targeting refining margins that had averaged 14 baht per liter. The measure expired on May 9, and prices have begun to rise again. The Oil Fund is now in a Bt60bn deficit, with diesel subsidies at one point exceeding Bt1bn per day.

The Ministry of Energy is seeking a Bt20bn loan to stabilize the fund, separate from the Bt400bn decree. Given Thailand’s heavy reliance on imported energy, the choice between absorbing more inflation and drawing down fiscal buffers is narrowing.

With the subsidy gone, margin pressure returns to fuel-sensitive sectors, including transport, logistics, and utilities.

5. Deflation ends with April CPI at 2.9%

After roughly 12 months of near-zero or negative readings, CPI inflation rose to 2.9% YoY in April 2026, the highest in 38 months and a sharp swing from −0.1% in March. The move was driven by domestic fuel prices linked to a Middle East supply disruption, which fed through to transport fares and prepared food costs. Core inflation rose to 0.8% YoY, its strongest reading in nine months. The Commerce Ministry expects May inflation to be around 3.1% and 2Q26 inflation to average 3.7%.

The key question is whether this marks a healthy return to the target band or the start of a stagflationary mix of rising prices and weak growth that would narrow policy options.

Looking ahead

Without de-escalation in the Middle East, Thailand’s outlook remains constrained by its reliance on imported energy. Growth is well below potential, inflation is rising due to supply-side factors, and fiscal buffers are being drawn down quickly. This is the environment Thai equities will have to navigate in the coming quarters.

But remember, the economy and the stock market, maybe a bit counterintuitively, often do not move in sync. One explanation is that the stock market is forward-looking, trying to predict what’s next, while economic data is typically lagging by months or quarters, attempting to explain what has already happened. A rising stock market when the economy is weak can signal a turning point.